All businesses, large and small can make use of an equipment lease as a way to increase cash flow and reduce liability. There are five basics that a small business can follow to get the best return from their equipment lease.

You own a small business, and you are looking at a lease as a way to gain access to needed equipment without incurring long term liability and to minimize reduced cash flow.

The simple equipment lease looks like the perfect vehicle to provide you with the needed equipment and keep the monthly payments lower than what you might pay with an outright purchase.

What Is A Lease?

The official definition of a lease is: a lease is an arrangement where the lessor agrees to allow the lessee to use an asset for a stated period of time. This is in exchange for one or more payments.

A finance lease is one in which the lessee assumes substantially all risks and rewards associated with the asset, while an operating lease is any lease other than a finance lease. International financial reporting standards.

Five Areas To Get The Most From Your Lease

An equipment lease is a valuable tool to get your business to profitability and stability. To be prepared and get the most out of any lease you should review the following five areas:

- Needs analysis

- Know the lease types

- Negotiate contract

- Impact on accounting and financial ratios

- What are the tax implications for each

1. What is Needs Analysis

The needs analysis is a process that is used by large and small businesses. It can be applied to all areas of the business where change can occur.

This can be used to help you gain a better understanding of the current requirements and also what your needs will be in the future.

This needs analysis can be conducted in four simple steps:

- Identify need category

- Business strategy

- Timeframe

- Goals

Needs Category

When you start a needs analysis for the acquisition of an asset the first step is to categorize the need. Example of need categories:

- critical operation

- cost reduction

- quality improvement

- a competitive advantage

- or a combination

After you have identified the need category it can help you determine, how much you may be willing to risk to get the equipment.

Identifying the category allows you to prioritize the resources you’ll need. For example, if you’ve categorized the need as critical, you’ll know you have to assign people and time to get this done.

On the other hand, if your category is a competitive advantage, you can be clear that you have to make sure that you can spend the time to do the research that the equipment you need and the way you finance it is in fact going to give you a competitive advantage.

Business Strategy

Once you have identified the need category does it line up with your business strategy? Your business strategy should guide each of your critical decisions.

If the decision is going to have a significant impact on labor, revenue, production then it should be aligned with the strategy.

A key to a successful strategy is when to say no.

There are two fundamental business strategies competing on cost or competing on quality. Any business that is in the marketplace and is not a charity then it is implementing one or both of these strategies as a conscious or as an unconscious strategic direction.

Competing on cost or quality requires dramatically different approaches.

Competing on price

To compete on cost means that you have a good sense of what competitors are charging, and what their margins are. For the low-cost strategy, you will put your prices below theirs.

To maintain your margins and profit you will have to be more efficient than your competitors. This may mean investing in better equipment for production. If your business is competing on price then you know all about volume and scale. Your equipment needs to scale up or down to meet demand.

Compete on Quality

To compete on quality means that you are focused on delivering the best possible product, and you are willing to charge more because you know your product is worth it.

This means that your production quality will need to be a step above the competition, your delivery will need to be at the top of its game. Your service after the sale stands above the competition.

Competing on quality often means you have repeat customers, you spend more to get a customer but you keep them, because no one else has a product that is as good as yours.

Make sure you know what your strategy is. Then does the new equipment purchase line up with your strategic goals? If it does great move on, if not stop and rethink why you are looking to acquire this new asset.

Your Timeframe

How quickly do you need to have access to the equipment? This can also help you decide what type of financing you’ll want to go with. As a rule of thumb, leasing tends to be quicker than a loan. But speed usually comes with increased cost.

Your Goals

What are your goals for the new equipment?

Do you know?

Have you put them down on paper?

If you’ve not done this stop right here and get them down. If you don’t you will lose a very valuable tool for assessment going forward.

Goals are critical they help you identify if you’ve made a good decision, track the performance, and figure out what needs to be adjusted going into the future.

When you decide on a goal make sure your following the SMART framework (Specific, Measurable, Attainable, Relevant, Time-Bound)

A famous quote from Peter Drucker “What gets measured gets done” Using the SMART framework for your goals allows you to measure performance and make adjustments as needed to reach your goals.

2. Know the Lease Types:

There are a number of different lease types that can be used for an equipment lease, the one that is decided on should match up with your needs analysis. Each lease type has different tax implications and responsibilities.

There are 4 basic types of leases.

- Operating lease

- Capital lease

- Leaseback

- TRAC Lease

Operating Equipment Lease

The operating lease is one of the most common types of equipment leases, and are often referred to as off-balance-sheet financing. It is a lease agreement in which the owner allows the user to use an asset for a time period that is shorter than the life of the asset.

Historically these have been the most popular types of leases because you can use them as off-balance-sheet financing. This provides some great advantages.

Unfortunately, the criteria for this classification have changed recently see Capital lease. In general, a lease can only be an operating lease if it is not classified as a capital lease.

General characteristics of an operating lease:

- The lessee only has a right to the asset during the lease period.

- The lease can be canceled at the option of the lessee

- Lease payment is treated as operating expenses

Advantages of operating lease

- leased assets are not listed on the balance sheet as an asset or liability.

- The debt-to-equity ratio (liabilities/equity) to appear lower

- The entire lease payment is treated as an operational expense.

- It may be possible to claim an abandonment deduction when removing the equipment to be replaced by new equipment.

Capital Equipment lease

Capital leases are now classified as finance leases under ASC 842 Also referred to as buyout leases.

This is a lease where the lessor only finances the leased asset. All rights of ownership transfer to the lessee.

These leases share the advantage of fixed monthly payments, but with the guaranteed option to purchase the equipment for a nominal price at the conclusion of the lease.

Advantages of using the capital lease are:

- Recognize expenses sooner than operating leases. The lessee can claim depreciation each year on the asset.

- The interest expense component of the lease payment can also be deducted as an operational expense.

- The end of the lease-purchase price of the equipment is known and agreed to at the start of the lease

4 guidelines that qualify a lease as a capital lease

Leases must be classified as a capital lease if it meets any of the following 4 guidelines as established by the Financial standards accounting board.

- Ownership: The lease transfers ownership of the property to the lessee by the end of the lease term.

- Bargain Price Option: The lease contains an option to purchase the leased property at a bargain price.

- Estimated Economic Life: The lease term is equal to or greater than 75 percent of the estimated economic life of the leased property.

- Fair Value: The present value of rental and other minimum lease payments, excluding that portion of the payments representing executory costs, equals or exceeds 90% of the fair market value of the leased property.

*3,4 do not apply if the beginning of the lease term is within the last 25 percent of the total estimated economic life of the leased property.

If none of these criteria are met and the lease agreement is only for a limited-time use of the asset, then it is an operating lease.

Equipment Leaseback

A leaseback or sale-leaseback transaction occurs when your business sells an asset it owns and then immediately leases that asset back from the new owner.

The seller “Lessee” and the buyer is the “Lessor”. This is a very effective way for a business that owns valuable fixed assets to access financing without involving traditional lenders, effectively generates cash flow without increasing debt.

A sale-leasebacks are attractive to lessees due to the transaction being treated as an off-balance sheet item. So this type of lease is classified as an operating lease.

This type of lease is common for industries that utilize high-value assets in the operation of their business. The perfect example of this would be the airline industry. They often purchase the asset then sell to a leasing company and lease it back to gain more working capital.

Equipment TRAC Lease

TRAC lease stands for Terminal Rental Adjustment Clause. This is a limited type of lease that by law can only be used for the financing of vehicles registered as over-the-road vehicles (autos, trucks & trailers).

This type of lease is usually entered into when a company would like to reduce its monthly payments to improve cash flow and an investor would like to reduce their tax liability or tax shelter.

In this agreement, the lessee and lessor agree to the residual value of an asset or the amount that the lessor will get at the end of the lease by selling or disposing of the asset.

If the asset is sold for more than the expected amount the lessee is credited the overage. If it is sold for less the lessee could be responsible for the difference. In most cases, the lessee can purchase the equipment at the agreed residual value at the end of the term.

An advantage of TRAC Lease is:

- the lessee can negotiate the residual value to increase monthly payments for a lower value at the end of the lease, or they pay lower monthly payments for a higher value at the end of the lease term.

TRAC Leases are the predominant form of leasing for large corporate fleets in the United States and Canada.

For accounting purposes, a TRAC is a capital lease for the lessee & finance for the lessor as an operating lease for the lessee.

Always check with your CPA when making any decisions based on tax liabilities.

3. Negotiate your lease

Depending on the lender your lease is open to negotiation. It is important to understand the limits of what you can ask for. Because of this, it may be worth it to work with experienced legal counsel negotiating leases.

If you are working with counsel or not your first step is to set your strategy for negotiations. A key part of the strategy is setting goals. If you have counsel work with them to set realistic goals and then compare those goals to your wants and needs.

Needs would be goals that are critical to moving forward, wants are those that would be great but if you don’t get them you can compromise on them.

Small businesses will begin to face increased requirements when seeking financing. Most equipment leasing lenders have watched the number of clients with bad debt and delinquencies more than double in 18 months. lenders are taking a closer look at which businesses they finance

Be clear about want and need. Understand what would be great to get and what do you have to have to proceed.

Forecasting equipment needs is not always easy, but a good idea of annual costs /- 15% is beneficial.

Understand how your company appears to lenders

Look at Dun & Bradstreet (D&B) credit report (check www.dnb.com) this will tell you what the lenders are looking at. Key info that they look at are:

- Time in business

- Ownership

- Lawsuits

- Liens

- Paydex score — this is a score that reflects how the business pays its bills. Scores under 50 are not likely to be approved.

Paydex is a score that tells the lender how your company is paying its bills compared to other similar businesses in your industry. Companies with a Paydex score under 50 will have a very hard time attaining financing. www.paynetonline.com

Know where you stand as a consumer

Most lenders expect the personal credit scores of business owners to be in the mid 650’s and most leasing companies have a hard cut off at 620.

The better your scores, the more leverage you will have with a potential lender or investor.

Make sure you comparison shop.

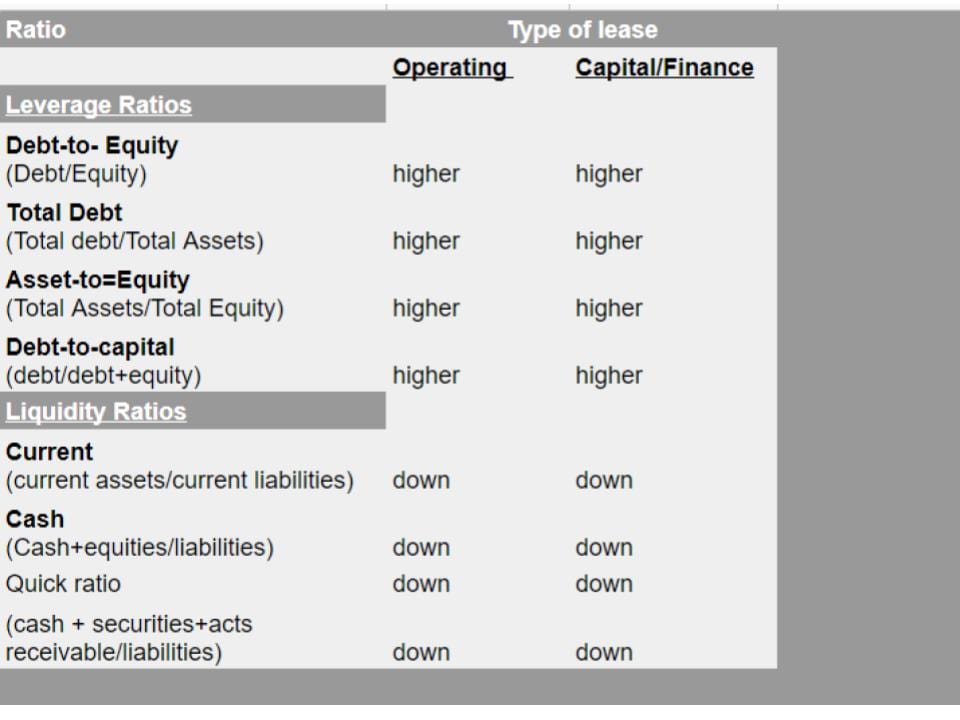

4. Impact on accounting and financial ratios

As of Jan 1 2021 (ASC 842) will go into effect. This is a new lease standard that all businesses must follow. The core principal is that a lessee will recognize assets and associated liabilities that arise from all leases.

The purpose of this change is to make business financials more transparent to potential lenders and investors.

The change affects key ratios and metrics that entities typically report to investors, lenders, and other key stakeholders.

ASC 842 will go into effect on January 1, 2021, make sure you are working with your accounting team to make sure you’re in compliance.

Effects of these changes on financial ratios related to leases:

5. What Are the Tax Implications for Each

In the recent past, the tax implications for capital or operating leases were known and straightforward. But as of the implementation of (ASC 842), the effects on your taxes have become more complicated. It is important to review how these changes will affect your business with your CPA.

Selecting the right type of lease that will provide you with the best and most optimum solution for your business is somewhat complicated. Given that a lease will likely encumber your business for at least a year, and in most cases longer, it is worth the effort to put together a team of advisors that would include senior management and legal counsel.

Make sure you compare and contrast to the Term Loan. A fixed asset that has a long lifespan can often be acquired more affordably than a lease.

If this is an asset with a long lifespan make sure to consider debt and equity financing.

Image by Free-Photos from Pixabay